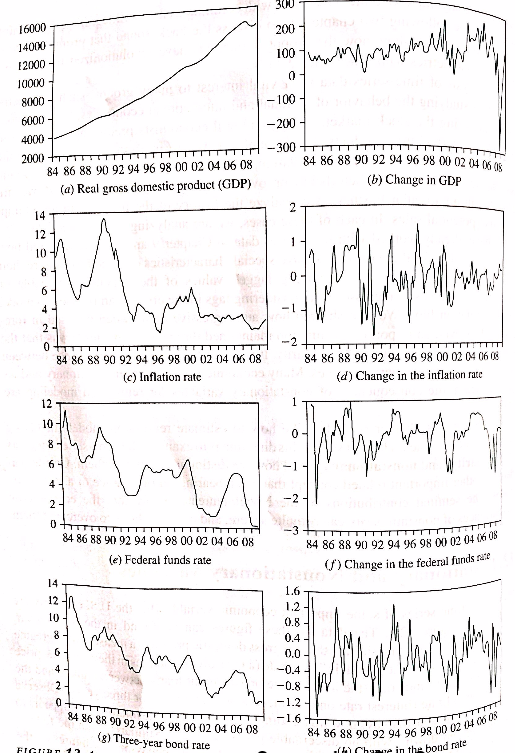

Time series yi is stationary if its mean and variance are constant over time, and if the covariance between two values from the series depends only on the length of time separating the two values, and not on the actual times at which the variables are observed.

Stationary: homoskedasticity

Nonstationary: heteroskedasticity

Stationary

|

Nonstationary

|

|

|

Stationary series have the property of mean reversion.

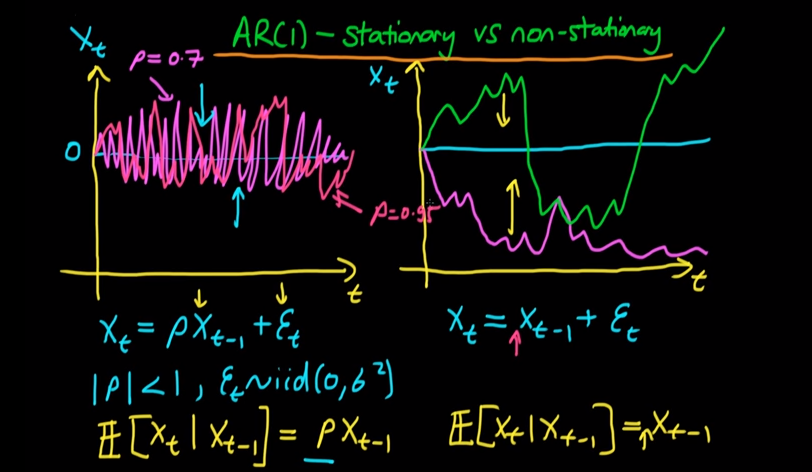

autoregressive model of order one, the AR(1) model, is a useful univariate time-series model for explaining the difference between stationary and nonstationary series.

Random Walk Models

These time series are called random walk models because they appear to wander slowly upward or downward with no real pattern; the values of sample means calculated from subsamples of observations will be dependent on the sample period. This is a characteristic of nonstationary series.

Spurious Regression: regression analysis is tha there is a danger of obtaining apparently significant regression results from unrelated data when nonstationary series are used in regression analysis.

The Breusch-Pagan/Godfrey/Koenker test

Mechanically very similar to White’s test. Checks if certain variables cause heterocedasticity. Consider the following heteroscedastic model:

Y = Xβ + u, ui ∼ normal, with E(u) = 0 and

V (ui) = h(α1 + α2Z2i + α3Z3i + . . . + αpZpi)

where h( ) is any positive function with two derivatives.

When α2 = . . . = αp = 0, V (ui) = h(α1), a constant!

Then, homoscedasticity ⇐⇒ H0 : α2 = α3 = . . . = αp = 0 ,and HA : α2 6= 0 ∨ α3 6= 0 ∨ . . . ∨ αp 6= 0.

When the Koeker test is statistically significant, as it is here, it indicates relationships between some or all of your explanatory variables and your dependent variable are non-stationary.

Unit Root Tests for Stationary: Dickey-Fuller Test

댓글 없음:

댓글 쓰기